Which metrics matter to drive your business strategy integrated with sustainability? What will the market see and understand? And what is the boards role?

This is a comprehensive blogpost, usable as reference for board members, relating to the sustainability measurement, disclosure and incentive topics. It initially explores some of the sustainability frameworks, regulations and rating providers, and then continues to the important actions boards can and must do.

For interested chairs and board member we invite you to join our upcoming board member peer exchange on June 10, where we will discuss boards practices related to measurement, disclosure and incentivization. Welcome to >> sign up for the board member peer exchange on June 10 at 10.15-11.45 CET

Table of Contents

There are many sustainability frameworks and regulations guiding disclosures – harmonization has started

An increasing number of standards and indicators are being used to assess, regulate and report (share) on sustainability and climate status and progress..

SDG, ESG, IIRC, CDP, SASB, TCFD, PRI, GRI, IFRS, ISSB, SBTi, EFRAG…. – Are you confused?

Many of these are inconsistent and thus can create more confusion than coherence within regulations and assessment providers, which is crucially needed to drive the critically required progress and support companies and boards on their transition journey.

A recent report Sustainability in the Spotlight: Board ESG oversight & Strategy [1] highlights that its primarily the full board that oversees ESG (43%). Boards are increasingly considering reconstructing the boards oversight of ESG (33%), likely because they aim to ensure that ESG goals and long-term strategy need to head toward greater alignment. However, more time, resources, and guidance are required for this, according to the report. It’s clear that more competence is needed, which is why some bring in external consultants (42%), and some provide training and special programs for boards (38%). Since some of this is overlapping, it’s interesting that some boards are not being provided with any additional sustainability training.

Sustainability Reporting Frameworks

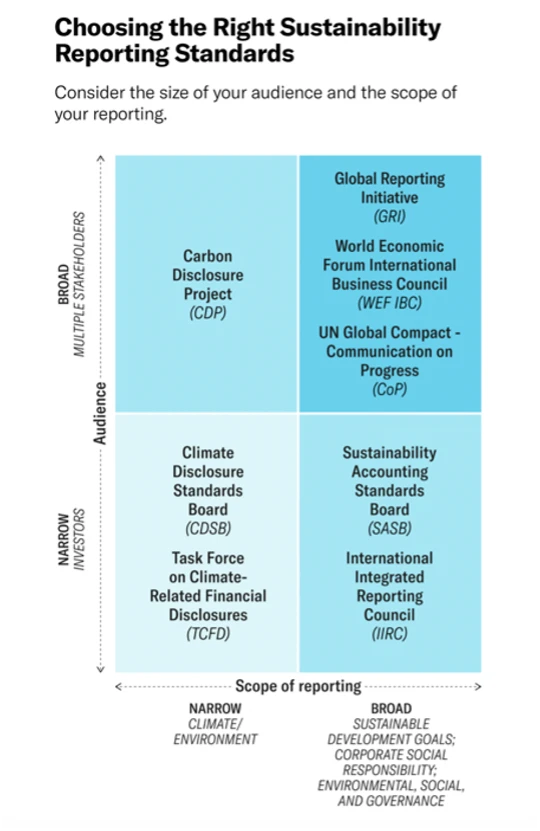

There is indeed an ongoing confusion with all the available Sustainability Reporting Frameworks available (sometimes referred to as the Sustainability Alphabet Soup, examples further below), with an approach to clarify in the Harvard Business Review article Designing your Company’s Sustainability Report [2] as illustrated in figure;

*Abbreviations and links for some in the Sustainability Alphabet Soup;

Note that some of the below are starting to merge and integrate

- SDG Sustainability Development Goals

- ESG Environment Social and Governance

- IIRC Integrated reporting

- CDP Carbon Disclosure Project

- SASB Value Reporting Foundation incl Sustainability Accounting Standards Board

- TCFD Task force on climate related financial disclosures

- PRI Principles for Responsible Investment

- GRI Global Reporting Initative

- IFRS International Financial Reporting Standards

- ISSB International Sustainability Standards Board

- SBTi Science Based Targets Initiative

- EFRAG European Financial Reporting Advisory Group

Sustainability Standards and Regulations

Another area in development are the standards and regulations, where there are three significant initiatives ongoing with regulation from Europe and US as well as an international standard;

- Europe Corporate Sustainability Directive, CSRD – ESRS, European Sustainability Reporting Standards (legal), including all ESG elements

- US Security and Exchange Commission SEC – Standardization of Climate-Related Disclosure for Investors (legal), including climate only

- Global International Finance Reporting Standards, IFRS- IFRS Sustainability Disclosure standards (standard), starting with climate and plans to expand to ESG

They currently unfortunately have a different basis for materiality evaluations, of scope and assurance measures. The good thing is that they are all basing their work in the climate area on Taskforce for Climate-Related Finance Disclosures, TCFD , which should help. There is currently ongoing market consultation on all of the three areas mentioned above.

Sustainability rating providers sharing conflicting assessments – creating some confusion and mistrust

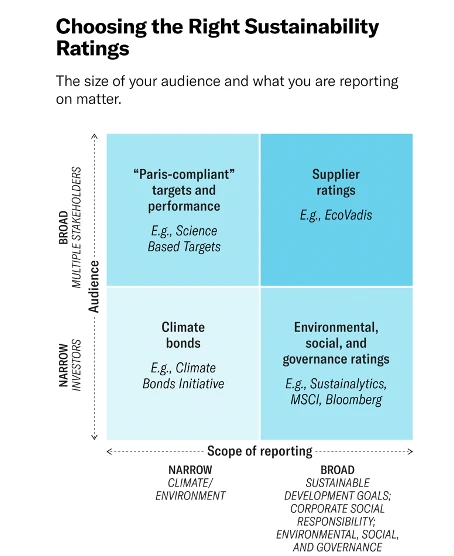

There is also ongoing confusion about the available Sustainability Rating Providers and why they share such different results, with an approach to clarify in the same HBR article Designing your Company’s Sustainability Report [2] as illustrated below.

The currently Most used Sustainability Rating Providers can be found in their article Top Rating Providers [4] to be MSCI ESG, Sustainalytics, Bloomberg ESG, FTSE Russell’s ESG, ISG Ratings and Rankings, CDP Scores, S&P Global ESG Scores, Moody’s ESG.

While there is an increasing voice of confusion and mistrust in the value of using the Sustainability Rating Providers, MIT has an entire research area aiming to put more light on the topic, as shared in their article: Why ESG rating differs, and what you do can do about it. MIT found that [5] “The ambiguity around ESG ratings is an impediment to prudent decision-making that would contribute to an environmentally sustainable and socially just economy” . MIT find the sources of the differences based on

- Scope divergence (fex when one agency includes ratings of greenhouse gas emissions, employee turnover, human rights, and corporate lobbying, while another doesn’t consider lobbying)

- Weight divergence (fex agencies assign varying degrees of importance to different attributes)

- Measurement divergence (fex measuring the same attribute using different indicators)

The resulting differences are alarming because it creates mistrust in the entire sustainability area and has such a major impact on companies and society.

Another insight on the topic comes from the company Clarity.ai which shares in their article EU Taxonomy: Using Tech to analyze “Green” Fund Performance [6] that they analyzed 31.000 equity funds using the EU taxonomy definitions and found that just one in ten funds has more than 10% green revenue.

…Or 90% of the equity funds have 90% of their revenues in non-green revenues….

A recent report ESG Global Study 2022[7], from Capital Group, that surveyed 1160 investors usage of ESG globally, including 60 from Nordics, found that investors 94% of European investors apply ESG, however 49% believe there is a perceived prevalence of greenwashing. The dominance is clear towards E with 48%, S with 27% and G with 25%, where the climate change is on top of the investors agenda.

Boards needs to act on sustainability and related metrics

So, what can companies’ leaders and boards do?

Boards needs to act on sustainability and related metrics

- Use WEF Climate Governance Principles to guide the climate and sustainability journey

- Form the board’s own view on company sustainability value creation, compliance impact and disclosure

- Create clarity by integrating sustainability and make impact areas comparable

- Share emerging board practices to speed up learning

- Make it personal – assess where you stand in your leadership to make it happen

Use the WEF Climate Governance Principles to guide the climate and sustainability journey

World Economic Forums Climate Governance Principles [7] are also a great guide for boards to reflect on. What the strategic impact of Sustainability and Climate issues means for the board’s accountability, competence, and structure of the board itself, how to assess materiality for both risks and opportunities and the integration into business strategy, and what to consider in reporting, disclosure, and incentives and how to meaningful exchange with stakeholders.

Boards need to ensure that they reflect on the board’s role and accountability, to make the strategy with related objectives and reporting based on an integrated material risk and opportunity assessment across the company. In the reporting space boards also need to ensure that the company reuse the insights and competence from the finance and internal control processes also for the sustainability data collection and reporting.

Before jumping into the reporting, it is crucial that the board considers what has most material impact on the business and what the business impacts most, across both business and sustainability risks. The key targets should preferably relate to improving risk and opportunities in those areas, integrated with the business strategy. As ONE comparison you can look at what others in your industry find most impacting, via an advisor or one of the rating companies. For example, MSCi provides an ESG Industry Materiality Map, here we can find that for a company operating in in different industries their most critical ESG material areas differ;

- IT Consulting and other services: E- Opportunities in Cleantech and Carbon Emission, S- Human Capital Development and Data Privacy & Security, G – Board, Business Ethics and Tax Transparency

- Real Estate – E-Opportunities in Green Building, S-Human Capital Development and G – Governance as above

- Food Retail – E- Raw Material Sourcing and Product Carbon Footprint, S-Product Safety, Data Privacy & Security and Labor Management and G – Governance as above

- Diversified Bank – E-Financing Environmental Impact, S- Human Capital Development, Consumer Financial Protection, Data Privacy & Security and Access to Finance, G – Governance as above

Another area to consider to include in the materiality revisit is the opportunity of circular resource impact and transition. In a collaboration with 30 companies World Business Council for Sustainable Development, WBCSD created the report Circular Transition Indicators 30.0 Metrics for business, by business[9]. They identified four steps to consider; Close the Loop, Optimize the Loop, Value the Loop and Impact of the Loop, with high level metric areas shown in figure below

Principles 6 and 7 explicitly guide boards around the reporting, disclosure and incentives, and can also be used for the broader sustainability area.

Where Principle 6 – focuses Incentivization – The board should ensure that executive incentives are aligned to promote the long-term prosperity of the company. The board may want to consider including climate-related targets and indicators in their executive incentive schemes, where appropriate. In markets where it is commonplace to extend variable incentives to non-executive directors, a similar approach can be considered.

Where Principle 7 – focuses Reporting and disclosure – The board should ensure that material climate-related risks, opportunities, and strategic decisions are consistently and transparently disclosed to all stakeholders – particularly to investors and, where required, regulators. Such disclosures should be made in financial filings, such as annual reports and accounts, and be subject to the same disclosure governance as financial reporting.

And WEF identified some helpful questions for a board for Principles 6 and 7 as

- How does our organization report on the material financial risks and opportunities associated with climate change?

- How do we hold management accountable for implementing the regulatory requirements for climate-relevant disclosure and for maintaining oversight of emerging regulations?

- Who in our organization is responsible, and how do we establish assurance?

- How is the management incentivization scheme designed to promote and reward sustainable value creation over time?

Companies Executives compensation schemes are increasing its focus on sustainability and ESG. An Executive Compensation Guidebook for Climate Transition[9] by Willis Towers Watson, highlights for example how Carbon Emission can be used as a metric, and shares related examples on how boards can design Long Term Incentives to motivate speed and overaccomplishment by using threshold, target and maximum levers.

Form the boards own view on company sustainability value creation, compliance impact and disclosure

”Leaders must understand the impact of ESG on an organization’s operating model, align themselves with stakeholders’ expectations and enforce a materiality assessment and reporting process.” – Laura Cha, Chair HKEX

From the ongoing Davos event, we got a summary by World Economic Forum about the challenge of lack of ESG standards and what is needed from leaders. The article

8 Leaders at Davos share how business can deliver on ESG promises [8]

shares that the lack of standardization on ESG scoring leads to confusion and advises on ways forward.

”Shift ESG considerations from compliance to value-creation by explicitly understanding how your company’s core business can concurrently contribute to social outcomes.” – John Schultz COO, HPE

As another guidance, they point to WEF’s work with auditing partners on Measuring Stakeholder Capitalism [9]. WEF identified 21 core ESG metrics that will help companies select and report on the pillars of principles of governance, planet, people, and prosperity. However, the key indicators need to be harmonized. See the related illustration below;

And taking the engagement and motivation further out in the organization and linking compensation to numerical targets for ESG priorities for all employees globally is done by Mastercard;

”With shared accountability, we can better connect the “why” of our purpose to the “what” of our fundamental business strategy” – Michael Froman, Vice Chair Mastercard

TCFD is also providing some guidance in the Report TCFD Guidance on Metrics, Targets and Transition Plans[3]. For a cross industry climate related metric categories, they identified GHG Emissions, Transition Risks, Physical Risks, Climate-related Opportunities, Capital Deployment, Internal Carbon Prices, and Remuneration.

Create clarity by integrating sustainability and make impact areas comparable

As boards and leadership teams are looking at the holistic picture of their business, it will help them have a more holistic view of the impact of their operations, related to both the traditional financial results and the impact of their sustainability imprints.

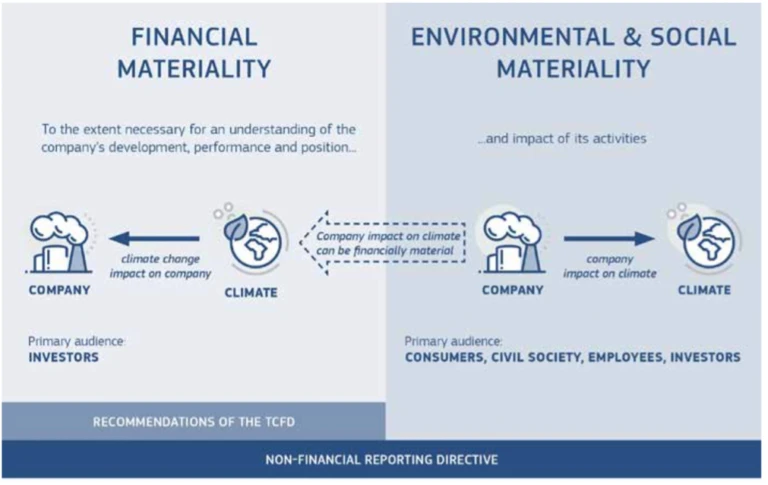

Several efforts are being explored to understand the impact of value creation further. The concept of double materiality is being explored, on how the sustainability impacts can be considered and even monetized in the same currency.

”Double materiality assessments enable leaders to regain focus by identifying a company’s key social and environmental impacts to be addressed.” – Daniel Schmid, CSO, SAP SE

Double materiality acknowledges that a company should report simultaneously on sustainability matters that are financial material in influencing business value and material to the market, the environment, and people. It is also defined in the EU sustainability regulation EU Double Materiality [10]

The concept of dynamic materiality acknowledges that the economic materiality of an issue can shift based on anticipated or unexpected circumstances. This was explained in a white paper from WEF “Embracing the new age of materiality harnessing the pace of change in ESG” [11]

Exploring the sustainability impact and double materiality is done in several emerging initiatives. The Value Balancing Alliance explores, together with a set of companies, how broader economic, social and environmental impact can be expressed in monetary terms. From their first Pilot Study [12] they share some of the insights from eleven of the companies that took part, including the impact in similar economic currency outlined below;

Another initiative is the Upright Platform– The platform shares some of the sustainability impact data in an open platform and is being used by another set of companies and investors. Similarly, they explore the broader impact with slightly different indicators and value in another way. An example from their platform below looking at the company Ericsson gives the below picture and insights

A company that has explored sustainability for more than ten years and is now sharing its fuller value creation model is the industrial conglomerate Linden Gruppen, headquartered in Sweden. Their ambition is to reach a more holistic value creation perspective and clarity, as can be seen below taken from Linden Gruppen 2021 Integrated annual Report [13]

Share emerging board practices to speed up learning

Join Boards Impact Forum to meet and learn with other board members. Or any of the chapters in your jurisdiction that are part of the Climate Governance Initiative.

Learn More and join our upcoming Board Member Peer Exchange

Board Member Peer Exchange June 10 at 10.15-11.45 CET

Boards Impact forums next Board Member Peer Exchange will focus on boards guidance and monitoring of the Sustainability Reporting, Disclosure, and Incentivization. The event will help you learn and exchange insights with other board members on the board’s role in company sustainability impact assessment, strategy adjustment, transition plans, reporting, disclosure, and incentivization.

The peer exchange starts with framing of the topic of Reporting, Disclosure, and Incentivization provided by Boards Impact Forum. We will use a poll to understand the broader perspectives of the participants, followed by group discussions and experience sharing, concluded with some mutual sharing.

Welcome to >> sign up for the board member peer exchange planned for June 10 at 10.15-11.45 CET

For insights on previous board member exchanges, read the summary from our first set of peer exchanges

Make it personal – assess where you stand in your leadership to make it happen

Board Member needs to make the approach, commitment and leadership relating to sustainability personal, and part of their Lifelong Learning.

Find support for personal development for modern Board Members and Leaders, specifically tailored to support the Sustainability Development Goals and based on the Inner Development Goals. The five key capabilities include Being, Thinking, Relating, Collaborating and Acting, and the development is supported by an Assessment, A Reflection Guide and A Personal Development Plan.

>> Personal Development for Board Members creating a Sustainable Future

References mentioned in the article with links:

[1] Spencer Stuart & Diligent, “Sustainability in the Spotlight: Board ESG oversight and Strategy,” 2022, [Online]. Available: https://www.diligentinstitute.com/research/sustainability-in-the-spotlight-board-esg-oversight-and-strategy/.

[2] Tim Rogmans and Karim El-Jisr, “Designing Your Company’s Sustainability Report,” Harv. Bus. Rev., 2022, [Online]. Available: https://hbr.org/2022/01/designing-your-companys-sustainability-report.

[3] TCFD, “TCFD Guidance on Metrics, Targets and Transition Plans,” 2021.

[4] Brokerchooser, “Most Common Sustainability Rating Providers (blogpost),” 2022, [Online]. Available: https://brokerchooser.com/how-to-invest/top-esg–rating-providers.

[5] T. Mayor, “Why ESG rating differs (and what you can do about it),” MIT, 2019, [Online]. Available: https://mitsloan.mit.edu/ideas-made-to-matter/why-esg-ratings-vary-so-widely-and-what-you-can-do-about-it.

[6] A. et al Pina, Bocquet, Boulet, “EU Taxonomy: Using Tech to Analyze ‘Green’ Fund Performance,” Clairity. AI website, 2022, [Online]. Available: https://clarity.ai/research-and-insights/eu-taxonomy-using-tech-to-analyze-green-fund-performance/.

[7] Capital Group, “ESG GLobal Study,” 2022. [Online]. Available: https://www.capitalgroup.com/content/dam/cgc/tenants/eacg/esg/global-study/esg-global-study-2022-full-report(en).pdf.

[8] WEF, “WEF Climate Governance Principles,” 2019. https://climate-governance.org/principles-for-effective-climate-governance/.

[9] WBCSD, “Circular Transition Indicators 30.0 Metrics for business, by business,” 2022. [Online]. Available: https://www.wbcsd.org/contentwbc/download/14172/204337/1.

[10] Willis Towers Watson, “An Executive Compensation Guidebook for Climate Transition,” 2021. https://www.wtwco.com/en-US/Insights/2021/11/executive-compensation-guidebook-for-climate-transition.

[11] S. Nayyar, “Business Leaders at Davos share how business can deliver on ESG promises,” World Econ. Forum, 2022, [Online]. Available: https://www.weforum.org/agenda/2022/05/business-leaders-at-davos-how-to-deliver-esg-promises-sustainability-reporting-standards/.

[12] WEF, “Measuring Stakeholder Capitalism,” 2020, [Online]. Available: https://www.weforum.org/reports/measuring-stakeholder-capitalism-towards-common-metrics-and-consistent-reporting-of-sustainable-value-creation/.

[13] European Commission, “EU Double Materiality,” 2019. [Online]. Available: https://ec.europa.eu/info/sites/default/files/business_economy_euro/company_reporting_and_auditing/documents/190618-climate-related-information-reporting-guidelines-overview_en.pdf.

[14] WEF, “Embracing the new age of materiality harnessing the pace of change in ESG,” 2020. https://www.weforum.org/whitepapers/embracing-the-new-age-of-materiality-harnessing-the-pace-of-change-in-esg/.

[15] V. B. Value Allliance, “Value Balancing Alliance Pilot Study,” 2019. https://www.value-balancing.com/en/downloads.html.

[16] LindenGruppen, “Linden Gruppen Integraed Annual Report 2021,” 2022. https://www.lindengruppen.com/sustainability-reports.

To learn more and join Boards Impact Forum

Upcoming webinars at Boards Impact Forum Our Events – Boards Impact Forum

Joining as a member or to receive the newsletter Join the Forum – Boards Impact Forum

Recent Comments